{kind=link}

A first-of-its-kind ‘State of the Industry Report’ by Material Innovation Initiative (MII) predicts that the global wholesale market size for next-gen materials will be approximately US$2.2 billion in 2026, representing a 3% share of $70 billion plus market.

MII is a San Francisco-based nonprofit organisation that works with startups, investors, brands, and scientists to accelerate the development of animal-free and sustainable materials.

MII research suggests that the next-gen materials industry will grow at 80% annually over the next 5 years as new materials begin to enter the market. The growth of next-gen materials will be driven by three factors: rapid advancements in science and technology, shifts in consumer preferences, and regulatory trends.

The new report for the first time analyses the growth of next-gen materials and highlights the opportunities that lie in developing technology and materials that inherently meet market demand for sustainability, style, and performance.

Need for next-gen materials and investment in the industry

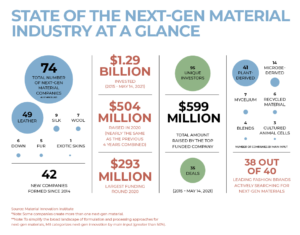

Today, most industries use conventional animal-derived materials such as leather, fur, silk, wool, down, and exotic skins. But the Covid-19 pandemic highlighted that raising animals for this purpose can be an uncertain business. The culling of millions of mink in fur farms to stop the spread of a Covid-19 in 2020 left the supply chain vulnerable.

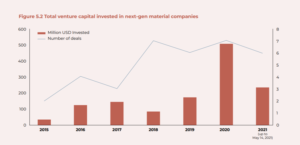

This could be one of the reasons why investment in next-gen material innovation reached new heights in 2020. The investment amount in 2020 alone is nearly the same as in the previous four years combined. Investment is expected to further increase as companies mature, demonstrate proof of concept, and scale, according to the report.

MII highlights that the next-gen materials industry is about 5-10 years behind the alternative protein industry, which grew massively in just a few years. Commenting on the same, Nicole Rawling, Co-Founder & Chief Executive Officer, MII, stated, “People who have missed the boat are now looking for the next Beyond Meat. I say look no further than the next-gen material industry. Next-gen materials are now where alternative protein was about 5 years ago.”

Next-gen materials are animal-free alternatives for conventional animal-based leather, silk, down, fur, wool, and exotic skins. These materials mimic the aesthetics and performance of their animal-derived counterparts. Besides these biologically derived materials, there are several recycled materials that are used in next-gen materials. Examples include plastic water bottles and textiles that can be repurposed into nonwoven fibres to produce next-gen down (e.g., Save The Duck) or yarns for next-gen wool (e.g., OSOMbrand).

Innovation in leather

Amongst all categories of next-gen materials, the one that attracts maximum attention are leather alternatives as this animal-derived fabric is most widely used in fashion, automotive, and home goods industries, with a global value of US$414 billion in 2017. Of the 74 companies considered in this report, 49 work on leather, which clearly forms the majority. Besides leather, nine focus on silk, seven on wool, five on fur, six on down, and one on exotic skins.

Although plant-derived materials have been the main input for leather alternatives, recently some companies have started using mycelium and microbe-derived materials to create their next-gen leather, such as MycoWorks, Mylium, MYCL, Neffa, Mogu, Malai, Karu, and Seevix Material Sciences.

What consumers say about next-gen materials?

A survey conducted by MII on US consumers reveals that although consumers find animal-based materials durable, they would willingly shift to alternatives to reduce their impact on environment and animals. This view is especially prominent among younger generations.

The survey also suggests that consumers are willing to pay more for products that align with their values but still meet their aesthetic and performance needs.

Surprisingly, 44% of consumers who prefer animal leather are willing to pay more for next-gen leather products and 20% of them are willing to pay at least 25% more than they are currently paying.

Big brands taking the sustainability route

With a shift in consumer preferences, established brands have started transitioning from animal-based materials to next-gen materials. While most of them source such materials from leading innovators in this space, some have created their own.

Big brands such as Nike, Adidas, Stella McCartney, H&M, GAP, Puma, Fossil, BMW, Bentley, IKEA, and others have specific targets to attain measurable improvements in sustainability. These new targets create concrete opportunities for material innovators as these brands are going to be the biggest buyers and users of their materials.

Innovating for the planet

With climate change and pandemics emerging as two of the biggest concerns today, the time is ripe to take swift actions to reduce our dependence on animal agriculture. Significant investments and partnerships are required to further the growth in next-gen material innovation. The report states that collaboration is the way forward, and now is the time to embrace sustainable innovation, both to create a liveable future on Earth and to create a prosperous future for the materials industry.

“If there’s anything I’ve learned from my time working with disruptive technologies, it’s that a rising tide lifts all boats. And in the next-gen materials industry, the tide is indeed rising,” said Rawling.

Read the full report here